As negotiations for a landmark UN Framework Convention on International Tax Cooperation enter a critical phase, the latest round of member state submissions expose the issues that have defined this process from the start and the new battlegrounds emerging ahead of August's fifth session in New York. The divide between Global North and Global South remains sharp, with developed countries pushing for a high-level, non-binding instrument that defers to existing OECD frameworks, while developing nations demand a treaty with real teeth and genuine reallocation of taxing rights.

María Emilia Mamberti, Research and Policy Lead, CESR

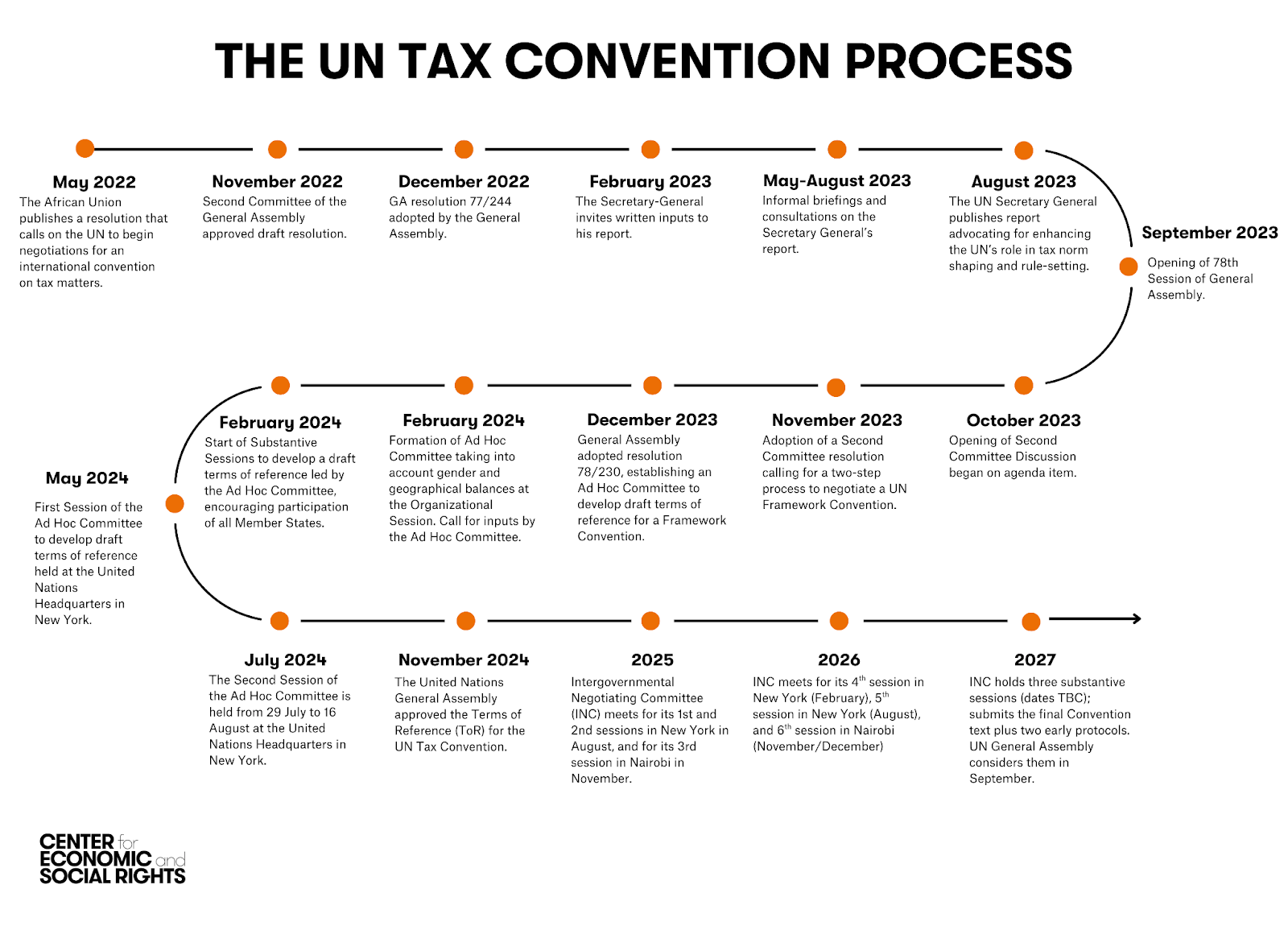

Negotiations for the UN Framework Convention on International Tax Cooperation (UNTC or the Convention) and two early protocols are reaching a peak point (for an overview of the process and its relevance, see our FAQs here). Within Workstream I, the track working on the Framework Convention itself, a full draft of the future treaty is expected to be published before member states meet again in New York in August for the 5th session of the Negotiating Committee.

In this scenario, States and other stakeholders have made a new round of written submissions to the process. A (regrettable) novelty is that States were able to opt for making their input confidential, not accessible to the public.

Here, we assess the latest submissions made by member States in connection with Workstream I on the Framework Convention (workstreams II and III focus, respectively, on the early protocols on taxation of cross-border services and dispute prevention and resolution) that are open to the public. These comprise 6 submissions from Global South members that are vocal in the process (Brazil, Indonesia, the Africa Group, and Algeria, Morocco and Nigeria individually). Other 16 submissions come from European countries, largely expressing similar positions, as we’ll discuss below. Two submissions come from some of the main blockers of the Convention (Israel and South Korea). The remaining submissions were made by Barbados, China, Saudi Arabia, Singapore, Türkiye, and the UAE.

The submissions restate many of the issues that have been at the core of negotiations so far, but also signal potential new negotiation paths and specific topics that will likely be prominent in future sessions. Below, we briefly survey first what the submissions indicate about the more established discussions, to then assess some emerging issues.

Recurrent themes

-

The Convention must be kept high-level. This is a common thread among all Global North countries' submissions. Implications of a high-level Convention are presented differently, with some countries interpreting it could only contain programmatic undertakings, and others arguing its provisions would have no legal consequences. Indeed, some propose “high level language” that instead of focusing on generality, suggests non-bindingness (for example, changing active verbs such as “develop” or “implement” for references to “endeavor to” or “recognize”). A brief analysis of the difference between high-level/not detailed and voluntary/non-binding is available here.

-

The Convention shall not duplicate existing frameworks. Global North countries also insist on the need to avoid duplication with existing work at the OECD. This is particularly salient on issues such as mutual administrative assistance, harmful tax practices, and exchange of information. As was the case during the last in-person sessions, some countries have asked developing countries for “clarification of the specific concerns” they have on the shortcomings of the present system. Several representatives of countries across Africa have responded eloquently to this (essentially, the shortcomings of the current system are what led to the negotiations of the Convention in the first place). Interestingly, and in connection with proposed article 10 on exchange of information, Brazil suggests language to mandate the Conference of the Parties to undertake periodic reviews of the mechanisms adopted to ensure they “...take into account the needs and capacities of developing countries…”.

-

Definitions and drafting of new articles. We again see repeated calls to promptly define terms such as “high-net-worth individuals”, “tax-related illicit financial flows” (in responses to this, see here), “harmful tax practices”, and, in some cases, “fair” allocation of taxing rights. Prompt development of article 15 on the relation of the Convention with other agreements is still a major priority, mostly for developed countries. Some countries are now also pushing for prompt development of the articles on reservations and the conference of the parties, and for a more fleshed out article on protocols.

-

Fair allocation of taxing rights (article 5). This is the core discussion in the Convention, and a clear divide remains here. Developing countries keep asserting their right to tax where economic activity occurs (for example, where assets or users are located, rather than where shell companies are registered), not necessarily requiring physical presence (such as a branch or office), to better account for current economic realities. They also normally oppose the current draft reference to "a portion of income" (to avoid the Convention share taxing rights by itself), and recognize the need to potentially renegotiate existing double taxation agreements (many of which can be biased against developing countries or even have colonial roots). Instead, developed countries call for a much less detailed commitment on allocation of taxing rights, arguing that the Convention should not itself function as an allocation rule, that the current draft does not reflect residency as a valid allocation criteria, and drawing a hard line on the call for renegotiation of existing bilateral treaties, which they reject on different grounds (that the Convention should not supersede bilateral treaties, that modification of bilateral treaties should be agreed between their parties, etc.).

-

High-net-worth individuals (article 6). While during the last session of the negotiating committee we saw large alignment on the “super-rich” commitment, in this round of inputs we again see concerns from several countries, essentially based on sovereignty (in some cases intertwined with administrative capacities concerns). These now add to privacy concerns over this commitment (raised most clearly by Luxemburg, Ireland, and Barbados). African countries are supportive of more ambition on the matter, proposing changes to the current text to use more mandatory language.

-

Mutual Administrative Assistance and Exchange of Information (articles 9 and 10). As before, on these matters we see special concern from Global North countries over non-duplication with current OECD work. More recent and nuanced comments from these countries focus on the need to keep language on “foreseeable relevance” for exchanging information, and on adding more robust privacy and data protection. Some further suggest complete deletion of the current article on exchange of information, and/or argue that the Convention should not itself be a legal basis for information exchange.

-

A procedural trick? As with the earlier wave of input, we saw repeated calls from Global North countries for more explanatory notes and legal and economic assessment of proposals. These remain, and now we see also demands for rapid intervention of the UN Office of Legal Affairs in the process. With a tone that curiously resonates with the way in which OECD work is often described (although used for a completely different scenario), Czechia went further to argue “negotiations so far have been ineffective and insufficiently transparent”. France similarly complained of “procedural shortcomings encountered since the outset” and asked that all issue notes “as well as all documents used (including those projected during the session), be transmitted at least one month in advance”. It is worth noting that these materials range from slides to 19 pages at most.

Emerging trends and issues

Development as a core of the convention, and its connection with gender, human rights, …and taxpayers rights?

Inputs related to the commitment on sustainable development might, at surface, show less convergence among all countries than they actually have. Many European countries and Brazil have argued for a more robust commitment, including references to human rights, gender, race, or the environment (in line with longstanding demands from CSOs). While the Africa Group largely expressed its preference for keeping the commitment as is, it did signal openness to making changes if they are aligned with some core principles. For instance, the Africa Group argued that if this article is to be "...further elaborated, it should be linked to domestic public resources, financing public services, reducing inequalities and supporting structural transformation in developing countries". Morocco eloquently added that “taxation is not merely a technical instrument but a central pillar of sustainable development”, and that this article should be aligned with the broader objectives of the United Nations, and guiding cooperation “by measurable development outcomes including those related to poverty reduction, strengthened domestic resource mobilization and sustainable infrastructure development…". The Africa Group has also been a defender of maintaining current language article 4 on sustainable development referring to States’ “different capacities” (which some European states rejected, despite this being the language of relevant earlier UNGA resolutions).

Also, we see alignment between a robust reading of article 4 on sustainable development and African countries’ proposals for a meaningful article 12 on capacity building and technical assistance. Both articles are at the core of making sustainable development a key goal of tax cooperation, moving away from mainly facilitating free-trade goals. Overall, these inputs may show more convergence among groups than initially apparent.

The reasons expressed in Morocco’s submission, or in an earlier UK’s input, are precisely the assumptions behind the concrete language proposals we recently made to the process with a group of leading human rights organizations. These proposals build on existing human rights’ norms and abundant UN human rights’ mechanisms interpretations to center the relevance of resource mobilization for rights’ realization, and the crucial role of tax cooperation in fulfilling economic, social and cultural rights.

In a few cases, however, we are concerned about the underlying intention behind proposals to introduce stronger sustainable development and human rights language for article 4. Italy and Norway, for instance, propose additions referring to “human rights, particularly taxpayers rights”. However, the connection between taxpayers’ rights and sustainable development in its social, economic and environmental dimension is not clear. We would argue that connection has never been actually established, and that such a reference would be inconsistent in article 4 (some of our work on these issues is available here and here).

Furthermore, while in Europe some taxpayers have argued cases defending their rights as taxpayers under fundamental rights protections, taxpayers rights are not a group particularly protected under international human rights law (and in other parts of the world, regional human rights bodies have not only not ever heard “taxpayers cases”, but more fundamentally do not engage with the rights of corporations). Taxpayer rights are an important issue, but they are primarily recognized in domestic law, in statutes, regulations, and often in administrative instruments such as taxpayer charters, revenue rulings, circulars, service standards, ombudsmen guidance or information published by revenue authorities; but not as a matter of international human rights law or sustainable development norms.

Indeed, the UK rightly differentiates between the content proposed on “human rights” for article 4 on sustainable development; and the content related to safeguards and “taxpayer and fundamental rights”, which according to the UK is relevant for the whole Convention but particularly for Articles 9 on Mutual Administrative Assistance and 10 on Exchange of Information.

Planting the seeds for future COPs

In our earlier blog, we discussed the relevance of the future conference of the parties (COP), the sort of activities a COP would ideally perform, and the need to include broad and concrete mandates for it in the Convention. The latest Africa Group submission eloquently proposes concrete language for COPs roles on harmful tax practices, mutual administrative assistance, and exchange of information. For example, it proposes the COP should establish criteria for monitoring and identifying emerging harmful tax practices, and determine what “effective taxation” means in this context. Similarly, on mutual administrative assistance and exchange of information, the submission proposes the COP develops guidance and protocol proposals. It is key that proposals as such are developed in connection with all commitments, beyond the drafting of a specific COP article.

Norway, the new influencer?

During the last in-person sessions, we saw Norway advance several text proposals, as the Africa Group and India did. The Norwegian proposals seem to have gotten a lot of uptake among European countries, who routinely referred to such text as acceptable in their inputs.

Concrete proposals are helpful tools to trigger honest and meaningful debates, and move the process forward. Yet all the proposals made by Norway for articles 5 (fair allocation of taxing rights), 6 (HNWIs), 7 (illicit financial flows), 8 (Harmful Tax Practices) and 9 (Mutual Administrative Assistance) -virtually all the core commitments of the Convention- implicate a subtle downgrade in the level of commitment of the treaty. For example, in connection with the proposal on article 5 (fair allocation of taxing rights), co-developed between Norway and Sweden, the latter openly recognized that one of the rationales is “to avoid potential implications for tax treaties”, protecting the status-quo. Lowering commitment is done through language proposals that change pro-active verbs (develop, implement, afford, eliminate) for non-committal verbs (recognize, consider, cooperate to enhance or to promote); the deletion of text providing guidelines for implementation; the replacement of concrete measures parties should undertake with mere examples of possible measures to be taken “as appropriate”; or the inclusion of clauses to act in conformity with existing norms.

The following chart provides some illustrative examples of these changes:

|

Article |

Current Text |

|

|

6 - HNWIS |

Commits parties to: - “develop and implement” measures to tackle tax abuse by HNWIs. -”explore” coordinated approaches to ensuring their effective taxation. -share information on structures and techniques used by them to avoid and evade taxes. |

Commits parties to: -”cooperate to enhance” measures to tackle tax abuse by HNWIs. -consider coordinated approaches to ensuring their effective taxation, respecting each State “flexibility to determine the design, structure and level of taxation” within its national tax system. The proposal does not commit any concrete measure, but mentions measures “may include, as appropriate”, exchange of experiences, practices, etc. |

|

7 - IFFs |

Commits States to: -”develop and implement measures” to combat tax-related IFFs. -ensure effective taxation of income and profits from such flows. |

Commits States to: -“cooperate to enhance measures” to combat tax-related IFFs. -ensure effective taxation of income and profits from such flows “in accordance with national laws.” |

|

9- Mutual administrative assistance |

Commits States to: -”afford one another the widest measure of mutual administrative assistance in tax matters” -cooperate to identify and eliminate administrative barriers that prevent effective mutual administrative assistance -act on requests for assistance as soon as possible, and promptly inform the reasons for denied requests |

Commits States to: -“cooperate to promote mutual administrative assistance in tax matters” - cooperate to identify administrative barriers that prevent effective mutual administrative assistance |

In the end, the issue goes back to the difference of high-level as general and not detailed, or high-level as non-binding or unenforceable, discussed above.

What's Next?

States and other stakeholders will regroup in person in less than five months, to continue work on the two early protocols and discuss a fully fleshed-out Convention template. The virtual, closed meetings that States will hold until then are therefore essential, and the round of submissions assessed here should provide vital input for the updated Convention draft, which we hope to see soon.